Differentiating capital and current expenditure

Image Source - Wikimedia Commons (https://commons.wikimedia.org/wiki/File%3AEverton_1933_FA_Cup_team_selection_ledger.JPG)

If anybody ever tells you that accounting is too simple, just ask him to tell you the difference between capital and current expenditure. In its full complexity, the question is and will always remain worth an argument. No surprises, then, that it is one of the most frequently litigated matter in tax matters that necessitate determination of taxable profits. Even at this very point of time, there are cases in courts on this matter.

Differentiating between capital and current expenses is one of the fundamental concepts of accountancy, apart from having a crucial implication for determining true profits, accounting disclosures and taxation liabilities. This difference is often codified in the relevant laws and accounting standards. For anyone attempting to do anything related to these fields must fully appreciate the difference between the two.

The most important difference between a CURRENT expense and a CAPITAL expense is that while the whole of the current expense is allowed as deduction from the receipts of business to compute the income from business, the capital expenses are not allowed fully as deduction. Its practical implication is that while a current expense will lead to lowering of profits as well as tax liability, the same will not happen in case of a capital expense.

Current expenses are also referred sometimes as revenue expenses. These are expenses undertaken directly, exclusively and wholly for the purpose of the business, without creating a lasting asset. In other words, current expenses are fully incurred for the day to the day running of the business.

Without these expenses it may not be possible for the business to earn a profit.

Examples of current expenses include payment of rent for office premises, electricity bills, salary payments of the staff employed in the office, expenses on stationary, gasoline used for office car, telephone expenses, repair of office furniture, transportation and courier payments. All these expenses are required for running the day to day activities of any business enterprise. One can see that none of these expenses create a lasting asset.

Current expenses do not create any benefit that will last beyond the year in which profits and tax liability are to be worked out. Since they are incurred for the business during the relevant year, and since they are not related with the profits of subsequent years, so the whole amount of these expenses is allowed as deduction from the business receipts for computing the profit of the business for the current year.

Capital expenses are those that create some lasting benefit or asset for the business, which will continue to help or aid the business activities beyond the current year in which profits are to be computed. Thus, these expenses are related with business profits of subsequent years too.

Typically, capital expenses are not incurred for day to day activities of the business. They usually create an asset which will usually last for a few years and help in business for all those years.

Examples of capital expenses include payment for purchasing a machine, or other office equipment, or the office premises itself. For a physician, purchase of blood chemical analyzer equipment will be a capital expense. For an author, purchase of a laptop will be a capital expense. For a restaurant, expenses for purchasing a large cooking range will be a capital expense. For a transporter, purchase of trucks will be a capital expense. For a pharmaceutical company, expense for purchasing a drug patent will be a capital expense. All these expenses create some asset that can be used for the business beyond the current year.

In some cases, a payment that gets rid of a liability can be a capital asset. For example, paying back of a loan by a company is a capital expense. Instead of creating an asset, it removes a liability from the balance sheet.

Since the benefit from capital expenses is not limited to the current year alone, and extends to subsequent years also, they are not fully deductible for computing the profits for the current year. Instead, they are allowed to be deducted from profits gradually, over the years, in the form of depreciation of an asset or amortization of other expenses. Sometimes, if the asset purchased by the capital expense is such that it does not lose its value with time, like land, then the capital expenditure may not be allowed as a deduction at all.

Capital expenses immediately impact the balance sheet, by converting one asset, i.e.. cash into another asset that is created from it. If the asset created is depreciable asset, it may lead to allowing of some depreciation as a deduction. On the other hand, current expenses do not directly impact the balance sheet, but are included as expenses or deductions in the profit & loss or the income & expenditure statements.

Capital expenses do not directly impact the profits and tax liability as much as the current expenses do. For this reason, there is sometimes a tendency for the business concerns to treat a capital expense as a current expense in their accounts. On the contrary, the tax administrators, like the I.R.S., will often want to verify if an expense shown as current expense is actually so or whether it might be a capital expense wrongly claimed as deduction. There can sometimes be a dispute between the two regarding the nature of the expense, which may have to be finally decided by the courts.

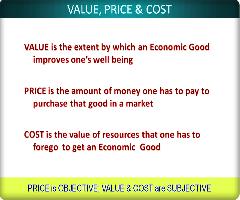

Price, cost, and value are separate ideas frequently employed in economics, commerce, and daily existence to elucidate various facets of products and services. Despite their interconnectedness, these concepts possess individualistic definitions and consequences..

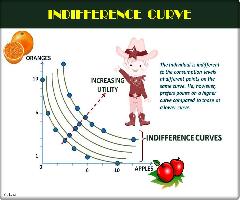

All economic activities including the most complex ones are finally aimed at consumption. However, to understand the kind of consumption that may be preferred by an individual, the concept of utility and indifference curve are extremely helpful.

Finance in a business is like blood in the body. Just as the body needs proper blood supply to be healthy and fit to work properly so does a business need funds to run successfully and to stand prosperously..