Tools and techniques of financial analysis

Image Source - https://pixabay.com/photo-2859651/

Financial analysis can be performed by employing a number of tools and techniques. In this article we will discuss some of the important tools and techniques of financial analysis.

Financial Analysis is defined as being a process of identifying financial strength and weakness of a business by establishing relationship between the elements of the balance sheet and the income statement. The information pertaining to the financial statements is of great importance through which interpretation and analysis is made. It is through the process of financial analysis that the key performance indicators, such as, liquidity solvency, profitability as well as the efficiency of operations of a business entity may be known, while short term and long term prospects of the business may be evaluated. Thus, identifying the weakness, the intent is to arrive at recommendations as well as forecasts for the future of a business entity.

Financial analysis focuses on the financial statements as they are a disclosure of a financial performance of a business entity. "A Financial Statement is an organized collection of data according to logical and consistent accounting procedures. Its purpose is to convey an understanding of some financial aspects of a business firm.

It may show assets position at a moment of time as in the case of balance sheet, or may reveal a series of activities over a given period of times, as in the case of an income statement." Since there is recurring need to evaluate the past performance, present financial position and the position of liquidity and to assist in forecasting the future prospective of the organization, various financial statements are to be examined in order that the forecast on the earnings may be made and the progress of the company be ascertained.

The financial statements are: The income statement, balance sheet, statement of earnings, statement of changes in financial position and the cash flow statement. The income statement, having been termed as profit and loss account is the most useful financial statement to enlighten what has happened to the business between the specified time intervals while showing, revenues, expenses gains and losses. Balance sheet is a statement which shows the financial position of a business at certain point of time. The distinction between income statement and the balance sheet is that the former is for a period and the latter indicates the financial position on a particular date. However, on the basis of financial statements, the objective of financial analysis is to draw information to facilitate decision making, to evaluate the strength and the weakness of a business, to determine the earning capacity, to provide insights on liquidity, solvency and profitability and to decide the future prospects of a business entity.

There are various types of Financial analysis. They are briefly mentioned herein: External analysis: The external analysis is done on the basis of published financial statements by those who do not have access to the accounting information, such as, stock holders, banks, creditors, and the general public. Internal Analysis: This type of analysis is done by the finance and accounting department. The objective of such analysis is to provide the information to the top management, while assisting in the decision making process. Short term Analysis: It is concerned with the working capital analysis. It involves the analysis of both current assets and current liabilities so that the cash position (liquidity) may be determined. Horizontal Analysis: The comparative financial statements are an example of horizontal analysis as it involves analysis of financial statements for a number of years. Horizontal analysis is also regarded as Dynamic Analysis. Vertical Analysis: it is performed when financial ratios are to be calculated for one year only. It is also called as static analysis.

An assortment of techniques is employed in analyzing financial statements. They are: Comparative Financial Statements, statement of changes in working capital, common size balance sheets and income statements, trend analysis and ratio analysis.

Comparative Financial Statements: It is an important method of analysis which is used to make comparison between two financial statements. Being a technique of horizontal analysis and applicable to both financial statements, income statement and balance sheet, it provides meaningful information when compared to the similar data of prior periods. The comparative statement of income statements enables to review the operational performance and to draw conclusions, whereas the balance sheets, presenting a change in the financial position during the period, show the effects of operations on the assets and liabilities. Thus, the absolute change from one period to another may be determined.

Statement of Changes in Working Capital: The objective of such analysis is to extract the information relating to working capital. The amount of net working capital is determined by deducting the total of current liabilities from the total of current assets. The statement of changes in working capital provides the information in relation to working capital between two financial periods.

Common Size Statements: The figures of financial statements are converted to percentages. It is performed by taking the total balance sheet as 100. The balance sheet items are expressed as the ratio of each asset to total assets and the ratio of each liability to total liabilities. Thus, it shows the relation of each component to the whole - Hence, the name common size.

Trend Analysis: It is an important tool of horizontal analysis. Under this analysis, ratios of different items of the financial statements for various periods are calculated and the comparison is made accordingly. The analysis over the prior years indicates the trend or direction. Trend analysis is a useful tool to know whether the financial health of a business entity is improving in the course of time or it is deteriorating.

Ratio Analysis: The most popular way to analyze the financial statements is computing ratios. It is an important and widely used tool of analysis of financial statements. While developing a meaningful relationship between the individual items or group of items of balance sheets and income statements, it highlights the key performance indicators, such as, liquidity, solvency and profitability of a business entity. The tool of ratio analysis performs in a way that it makes the process of comprehension of financial statements simpler, at the same time, it reveals a lot about the changes in the financial condition of a business entity.

Last but not least, financial analysis is a continuous process being applicable to every business to evaluate its past performance and current financial position. It is useful in various situations to provide managers the information that is needed for critical decisions. The process of financial analysis provides the information about the ability of a business entity to earn income while sustaining both short term and long term growth.

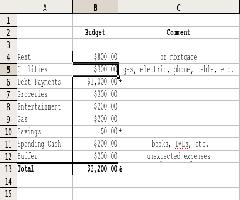

Excel templates to plan your budget is wise because Excel calculates your budget for you and you will have a personal template that can be updated monthly. When changes are made Excel automatically recalculates your totals on your spreadsheet so that it does all the hard work and all you do is save your new budget template..

In order to become a very successful entrepreneur, you would need to have certain very important skills. These skills when applied in the right way can make you the best entrepreneur..

Network marketing also known as MLM, have been a major home business many take part in, however to success in it there are several attributes, ideas and means you must adopt and practice..