How to become an Economic expert of your home

Image Source - https://pixabay.com/photo-2504417/

This article includes the basic financial economics an individual faces on a daily basis, irrespective of the country he or she is living in. The sooner this knowledge is learned and shared, the better for you.

Difference between ‘Need’ and ‘Want’

Theoritically speaking, the words ‘need’ and ‘want’ almost sound synonymous. We, as people, tend to use the words interchangeably without knowning its actual meaning. But, in reality, there is a hair line difference between the words. The difference is a significant one. The word ‘Need’ is something one cannot live without and the word ‘Want’ is something one craves for at that particular time. For example: eating food, drinking water and staying under a shelter can be categorized under ‘Need’.

But eating food in a restaurant, having a cold drink and staying in a hotel can fall under ‘Want’.

According to economics, the word ‘Need’ is rightly defined as something without which it would become difficult for one to survive, either in physical form or a society while ‘Want’ is defined as something one desires. Usually there are two forms of ‘Need’ - Objective and Subjective. Objective needs include food, water, clothes and air while subjective need include intangible items like a sense of self-respect and security, without which it would be impossible to survive in society.

Unlike economics, the definition of needs and wants differ from person to person because it is directly linked with one’s purchasing power and bank balance. A typical middle class person earning $35,000 a year would be satisfied with basic things, which is defined under economics. However, definition of the same basic things will change for a person who earns $100,000 a year. Fundamentally, the functions of the things will remain the same, however, it will be far more expensive than the basic ones.

Let’s go outside the personal life in the corportate world. Many a times one might have heard this – “I want this by afternoon evening” or “ I need you to do this over the weekend”. Here also there is different interpretation of words ‘need’ and ‘want’. In this context ‘need’ signifies the importance of the work or duty that has assigned. The importance of the work or duty is directly linked with the team’s or company’s performance. However, usage of the word ‘want’ implies one’s wish, and not importance, towards completing the job or duty.

Before making any purchase or giving orders it is very important to ask this question to oneself – “ Do I ‘need’ this or do I ‘want’ this?” If the answer comes out as ‘Need’ go ahead and purchase it but if the answer is otherwise; wait till the time it becomes a ‘Need’. In the meantime, save that money or utilize to satisfy other needs. If one follows this policy over a period of time it would be observed that one has managed to save a significant amount which can be used for a better future. In the corporate world too, if the intrinsic meaning of words is used there might be a significant positive change in the team’s or company’s performance.

How to save money?

If the World Bank is to be followed then global savings rate in the last decade is gradually declining. This declination has led to a domino effect ultimately resulting in people defaulting on their debts or compromising on their needs. A renowned investor, Warren Buffet, has always said “every penny saved is every penny earned”. This statement is true to its every word because it is the savings that becomes your umbrella on a rainy day. It doesn’t matter if an individual is earning in thousands or millions, if a significant proportion of income is not saved then their lives can litrelly turn upside down when it is confronted with a crisis of any nature. Saving money as a duty might take you off-track later on, but making it a habit might make it last for generations.

There are various ways or methods to save money. Systematic saving, following discipline while spending and commitment towards fulfilling needs (and not wants) is the key to save money. Let’s have a look at few methods that may help you save.

Traditional Method

Given any day, one’s pocket or wallet would usually have change in coins at the end of the day. Bring 2-3 small piggy banks and place it in different corners of the house. Make a habit of depositng these coins in a piggy bank. And when the amount becomes huge, deposit the money in savings account. Again repeat the process. This way, even without an impact on one’s monthly income, an individual can save a handsome sum over a period of time.

Deposits in banks

There many options to save monies when it comes to savings in bank. Apart from a normal savings account, one can go for term deposit or opening a retirement fund. However, while going for these deposits it is very important to ensure that the bank is providing competitive interest rates. Banking products like term deposits and retirement fund will automatically deduct money from salary cheque, thus ensuring savings (even if it is forgotten) for a better future. While term deposit will ensure high interest rate than normal savings account, retirement fund will take care of the needs when the income channel is close for good.

In case, a person is concerned about the tax portion then options like Tax Free Savings Account (TFSA) and Register Retirement Savings Plan (RRSP) are always available. While opting for these kind of accounts or deposits it is usually advisable to consult a tax expert or a financial planner.

Apart from the above mentioned types, it is always great to dedicate one protion of the monthly salary towards the savings account. Although slowly and gradually, over a period of years, the bank balance will look huge.

Example:

Let’s assume a person’s salary is $35,000 annually and every year 20% or $7,000 is being deposited in the savings account. Now, assuming the work tenure to be 20 years, excluding interest the bank balance will stand at $140,000. This amount can be utilized in covering childern’s tuition fee or even investing in real estate.

Creating an effective budget

Ensuring an effective and effiecient budget is the key to prosperous savings for the future. Cutting down budget while maintaining perfect balance between needs and wants can be termed as an efficient one. One needs to take few strong steps, alter some habits and adjust a little. This will lead to an effecitive budget. It’s a psychological workout. One must prepare itself mentally to control expenditure, which automatically means saving more.

Work on a budget

The very first step is to take pen and paper and start noting down daily expenses. This habit will help realize the difference between the need and want. Shunning the wants and focusing on needs will help one draw a blueprint of the monthly expenditure. Make sure to include all the expenses of all your family members in the list irrespective of it being big or small. Take note of any debts, loans or fixed expenses like rent, mortgage or interest while drawing up a monthly budget. Over and above planning the budget it is very important for the family to follow it dedicatedly. It is only then, the results of budget being an effective one will be seen. After creating a small space for savings and drawing up the budget, one can have the liberty to become a little thrifty.

Stop wastage

A budget can become an effective one when importance is given to controlling expenses. Controlling expenses include optimum use of gas, electricity, grocery, etc. Make a habit of turning off the main switches of appliances like television, grinder, air conditioner, microwave, desktops. Do not use products that take long time to heat or cool down. Repair electronics on time to avoid such circumstances. Unplug your mobile phones, laptops, etc. once they are charged and use the charger provided with your device only. Do not over charge them. Turning off lights when not in a room will save a lot in the electric bill. Use efficient and low power consuming fans and bulbs. These are very small things that usually go unnoticed. If these are given importance, it can make significant positive changes in one’s monthly expenditure.

Another avenue that can make budget more friendly is the usage of mobile internet and telephone bills. Buying a group plan for family and friends is advisable as it usually comes with free voice calls. Manually switch off your data connection when not in use, avoid trusting your mobile for such automatic settings.

Creating a disciplined budget does not mean becoming stingy. It means allocating appropriate money for right purposes to fulfil the needs of a family, thus encouraging savings on the sidelines.

Understanding the term ‘Value’

Value is a simple word to understand but to grasp its meaning it is important to know the meaning of price. Let’s take an example to understand the difference.

Supposedly one goes to a shopping mall and accidentally encounters his/her favourite t-shirt of a particular brand which is priced at $20. The person immediately shells out the money and buys the t-shirt. Here, the person has paid the price of $20 to purchase the t-shirt. However, the value of that t-shirt is completely different for the person. Why? Because it is his/her favourite.

Now let’s take another example, a little bit different from the above one.

Let’s say a person decides to invest $1,000 in stock market. He buys 100 shares of one particular stock and keeps it for 10 years. Over that particular tenure, he gets consistent dividends in addition to 1:1 bonus shares. In this case, the price he paid for 100 shares was just $1,000 but he got the value in terms of dividend and bonus shares.

Price is usually defined in monetary terms, however, value is something that can be measured in terms of emotions and incentives. It is really important to understand the correlation between need, want and value. Price is something which you will ultimately pay, hence, it can be termed as a constant. However, if the price is paid for a need then the chances of an individual receiving its value of a period of time increases significantly.

On the contrary, if one pays price for a want then the nature of its value will last for a short term. Hence, it is very important to ascertain and prioritize the purpose of price which one is willing to pay.

It is hard to believe but technically speaking, the value of $100 bill is never same even the very next month. Wondering how? Well, if one considers an annual inflation of even 1% (for example) then on a monthly basis the inflation will turn up to be 0.0833%. Hence, the value of the $100 bill increases to $100.0833 the very next month.

Thus it is of utmost importance to know the impact and value of the good or product for which one is willing to pay a price for. The one and only criteria for paying a price should be that the product which is bought should provide value for long term. Even while preparing a budget, if the items listed has great value, the budget will automatically turn out to be an efficient one.

How to get rid of debts/loans

Although people usually maintain the fact that it is advisable to stay away from debts and loans, it remains a hard truth that at some point of time in life one has to approach banks for loans. Usually loans are taken for business, studies, medical reasons or purchasing a home. Agreed that interest rates might differ according to the nature of loan, the very presence of an outstanding debt has the potential to upset an effective budget, atleast for a middle-class person.

In a bid to avoid this kind of situation, it is advisable to take stock of the situation well in advance so that it doesn’t hamper the future. The first and foremost thing to do is calculate the number of interests and principal left. After calculating the outstanding debt, ensure that the respective amount due is always available in your account on the due date. In case the amount is not ready, make sure to keep one portion of the salary cheque dedicated towards the loan or debt. The faster the loan is paid, the better becomes the financial stability.

If at some point of time, one gets a lumpsum in form of a work bonus or a term deposit, make sure to pay off the debt immediately. This way one’s finances can be saved from the interest’s burden. If not paid off, a lump sum payment towards the loan will at least lower the interests in future.

While making sure to pay off timely debts, try to cut unnecessary expenses. These may include going to restaurants, watching movies in multiplexes, over-using the credit card, unwanted shopping etc. These expenses are small, no doubt, but aggregately these can offset the monthly interest payments.

With loan or debt on your side ensure that there is no shortage of income flow. This is because the monthly interest tend to spoil the budget which leads to compromise in needs. In a family of four, if one person is earning try and up the number to two with the help of an extra shift or job. An additional flow of income will definitely offset the interest payments.

There are times when one tends to avoid loan or debts. It is the last thing one should ever do. Be informed the that the nature or loans and debts are such that if not paid within time, it’s interest gets compounded which in turn makes life more difficult. So avoiding it or running away from it never an option.

In a worst case scenario if one cannot pay off loans or debt, approach the bank itself and explain the whole situation. There are a number of options offered to the debtor through which they can restructure the entire debt. These may include extention of deadline along with lower interest rate or selling of a property owned by the debtor.

In any case it is best to never take a loan and if a need arises it is better to discuss with the family first because its effect tends to directly influence the monthly budget. It is only after preparing a plan to pay-off the loan, one should approach a bank for loan at attractive interests.

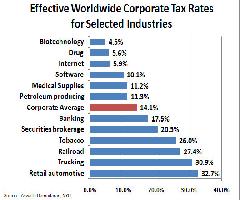

Tax is one of the most sensitive topics in public discourse. One of the most common public demand of the ordinary masses is tax rebate.

Harsh economic environments can have adverse effects on your business, however, there are some important practices that can ensure that your business survives. .

As the whole world gets integrated into a single global market, the greatest challenge for all business enterprises is to find and tap new international business opportunities. However, it is a task full of various challenges, some related to attitude and others to technology.