Individual as well as Public Actions are dependent upon the Interaction of Value and Costs

Image Source - Image created and owned by the author, V Kumar.

Basic economics requires conceptual clarity. Most economic decisions at the level of individual economic agents are a function of value and cost of an economic good for them. Buying and consequent consumption results from value exceeding costs. Transfer of resources undertaken through taxes and subsidy must be taken at the level of the Government, and are always a challenge in public policy.

Once the distinction between value, price and cost becomes clear, it is not difficult to make out how and why people decide to indulge in economic actions in respect of economic goods. The decision could be in favor of any one of the four basic economic actions of consumption, production, exchange or transfer. Most economic studies rely upon these basic principles to predict how a particular intervention by the Government will affect the national economy, or what needs to be done by the Government to achieve a particular economic outcome.

Consumption is always by a human being, and aimed at making his life better off. This improvement in his well-being reflects the value of a particular economic good for that individual. On the other hand what he would have to forego to obtain that good would be his cost, and would include what he may have to give away as well as what he has to miss out upon.

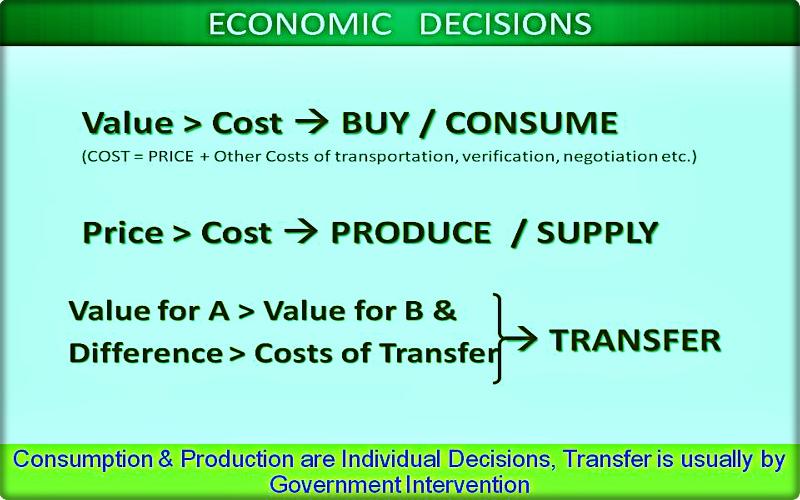

Value and cost are the fundamental aspects of any economic good. Value is the benefit that a human being gains from a good, while the cost is the benefit that is given away in producing or buying it.

A buyer will be willing to buy if the cost of that good for her is less than the value of that good for her.

Here it is important to remember the distinction between cost and price. Cost of buying a good will include not only the price but also other expenses like transportation of the good, the opportunity cost of time likely to be spent in searching for that good, verifying whether it is good enough and negotiating for it. Each of these costs affects a buying decision in addition to price. For instance, in some online sales, the cost of a good is low enough to make it look an attractive bargain, but the high cost of its delivery may still deter the customers from buying it. Similarly, a product that is not easily available may not be bought in spite of its high value and low price. Sometimes people do not buy a product if it is difficult to verify its quality, and as an alternative, they are willing to pay a premium for getting an assurance of quality, as in case of a well known branded product. Difficulty in verifying quality is often the biggest cause of high discount on used products.

Of course, the most important determinant of a buying decision is price, which is the amount of resources that is exchanged between the buyer and the seller, and for most purposes, is taken as a proxy indicator of the value and the cost. The willingness of a consumer to pay for a good reflects his individual demand for that good. The total demand of all consumers for a particular good reflects the demand for that good in the economy. The total demand for all the goods in the economy is known as the Aggregate Demand.

After the preceding discussion, it is self apparent that a producer will be willing to produce or supply a product, if the price he is likely to get in an open market is more than the cost that he would need to incur for producing or procuring and supplying that good. This is also the underlying principle for market efficiency in allocation of resources. A good should be produced by the society if its value is more than the cost of producing it.

Since the actual price will be known only at the time of sale, the producer needs to make a future prediction about the likely prices that he would be able to obtain. This involves an estimate based on expectations. When the economy is doing well, producers expect to get a good price for their produce and hence tend to produce more. However, if there is an economic downturn, and people become conservative in their expenditure, the resultant fall in demand can lead to surplus production. In such cases, producers can either keep large inventories or sell at a discount.

Decision of consumption, production and exchange of goods are generally taken at the level of individual economic agents, but the decision for transfer of goods, which mainly consist of taxes and subsidies are taken by the Government, which collects resources first by way of taxes and then distributes those resources to the needy by way of subsidy. Such transfer of resources would be justified only when the resultant addition in social welfare is more than the costs to the society of the same. It is generally one of the most difficult decisions, and ideally should be undertaken only after an elaborate cost benefit analysis.

For a public administrator or a policy maker, understanding the difference between value, price and cost is a must, because the policies of the government are usually oriented to bring some benefit to the people, and unless the administrator is able to understand and estimate this benefit, it may not be possible to plan efficient policies. It is also important that the value of a good or a service for a person may be different from the value of that same good or service for another person. While framing its policies, it is essential that policy makers are aware of value that the policies would create for the beneficiaries.

It is equally important for a public administrator or a policy maker to understand the concept of cost. Government policies, especially the regulations can create a lot of costs for the people, even when the Government may not be charging any money from the people. Let us consider an example, where Government regulation makes it mandatory that every person buying a Television must first register with a Government office and take a license. Even if the Government does not charge any fees for such license, this policy will still impose significant costs on the people, since it requires that a person wanting to buy a Television must first apply for a license. Further, if there are too many people seeking this license, and not enough officials dealing with it, the applicants will need to come to the office and enquire about their application again and again. Every time a person comes to the office, it incurs costs in terms of time, effort and transportation. The more the delay in issuing the license, higher will be the costs. Since, this policy entails significant costs on society, it should be applied only if the benefits of such a policy exceed those costs.

Personal budgeting helps in managing personal finances. It helps in making proper plans related to money and provides an effective way to control our expenses.This article discusses the importance and benefits of maintaining a personal budget..

Indiscipline, is lack of control or discipline. It’s violation of some established and definite rules or moral code.

Budgets are an integral part of running any business in a successful manner. Effective budgeting system is a key to organizational success.