What is that distinguishes them all?

Image Source - Image created and owned by the Author, V Kumar

Price, cost, and value are separate ideas frequently employed in economics, commerce, and daily existence to elucidate various facets of products and services. Despite their interconnectedness, these concepts possess individualistic definitions and consequences.

In common parlance, people often tend to use the words value, cost and price as synonyms. Understanding how they differ is the first step towards understanding economics. The relevance and importance of this difference can be understood by the fact that economic behavior of economic agents in respect of a particular economic good is governed to a great extent between the difference in value, cost and price of that economic good for that economic agent. Understanding this basic principle is particularly essential for public managers studying economics.

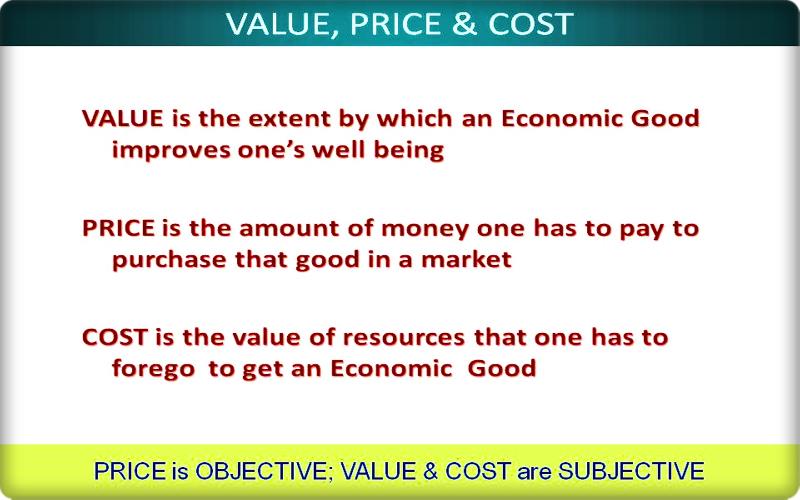

Value of an economic good for an economic agent is the extent to which it improves its well being. It is often referred to as utility in welfare economics, representing the value of a good for a human being. For example, if you are hungry and you get a sandwich, the extent to which that sandwich can make you better off is the value of that sandwich.

Similarly, if you are feeling thirsty, the extent to which a drink makes you better off is the value of that drink. The value of any other good can be understood from the extent it makes one better off.

The most important aspect of value that one needs to understand is that the value of a good is not constant. It differs not only from person to person, but may also vary for the same person from time to time. For example, if David likes apples and John doesn't, then the value of an apple for David will be more than the value of that apple for John. Now, suppose that John likes oranges and David doesn't. So if it so happens that David has an orange and John has an apple, and both come across each other, it is possible that they may end up exchanging David's orange for John's apple, and by doing so, both of them will be better off. Note that such an exchange will mean an increase in the value of the apple as well as the orange. If we define social welfare as the well-being of David and John, this orange-apple exchange increases that social welfare.

Interestingly, the value of a good for the same person may also keep changing. Imagine that value of a sandwich for you at a time when you very hungry. Now compare it with the value that the same sandwich may have for you just after you have had a very sumptuous meal. The value of sandwich depends upon how badly you want it, which in turns depend upon whether you are hungry or not. The value of a medicine for a person may be much more when she is sick compared to when she is well and in good health. The value of a good may also depend upon other factors that determine its usefulness. For example, a room heater may have a lot more value during winter season, compared to its value during summer. Same would be true for warm clothing too.

Artificial persons like a company do not consume any good, and so in their case, the value of a good is directly linked with any financial improvement or profitability that such a good can bring it. For instance, a machine can reduce production costs and thereby improve profitability, or it may be an intermediate good that is then transformed into a final good that can be sold off at a profit. For a trading enterprise, the value of a good would simply be the price it can fetch on resale.

Value of a good is what determines whether someone wants to have it or not. It also determines how much that someone may be willing to give up in exchange for that good. Thus, value of a good is the primary determinant of how much of that good is wanted by whom. Value is the primary determinant of the quantity of that good's consumption and production.

Price is what a buyer pays to a seller. Unlike value and cost, price is common for the buyer and the seller. It is the amount of money or the amount of real resources that are exchanged between the buyer and the seller as a consideration for that good. In a free and open market, the price of a good is determined by the demand and supply of that good.

An important aspect worth noting is that price of a good may be different from the value of that good for the buyer, and the cost of that good for the seller. Even more important is the fact that the price is driven by demand and supply, which in turn are driven by the value of that good for the buyer, and the cost of producing and selling it for the seller, respectively.

Price is thus determined by the value and the cost of that good. Being the only objective and measurable factor, price is the one which is often used for accounting, planning, management and administration. Not only that, since the value and cost of a good are subjective and difficult to measure accurately, price is also taken as an indicator or a proxy for determining the value and cost of that good for the society at large.

It may be useful to remember that economics and finance are different. In finance, the cost of a good is the money paid for buying it. However, in economics, cost of a good is the amount of your well being (utility) or your resources that you have to give up, for getting that good. If you have to buy that good in the market, then you will have to pay the market price to the seller. However, to buy that good, you will have to give up some resources in addition to the price that you pay. If the shop of the seller is ten miles away, then the time, effort and money that you spend in going to that shop is also a part of the cost of that good. Measuring these resources is essential to quantify the cost you have to bear to get the good.

Understanding cost is a fundamental aspect of economics, and understanding it is essential for achieving economic efficiency. It includes not only the actual resources that are given up but also the potential resources which are given up by opting for a particular good. For example, if you go to watch a movie when you could have alternatively worked somewhere and earned $100, then the cost of watching the movie includes not only the price that you pay for the movie ticket and the price of transportation to the Movie Hall and back, but also the $100 that you could have possibly earned, but could not because of your decision to go and watch the movie.

There are four basic economic actions that a person can indulge in respect of economic goods. All these actions by any economic agent are largely governed by the interaction of value, price and cost of that good for him.

Thus, it is essential to understand the distinction between these three closely related terms.

If anybody ever tells you that accounting is too simple, just ask him to tell you the difference between capital and current expenditure. In its full complexity, the question is and will always remain worth an argument.

The bottom of the pyramid strategy has now been extended to other sections of society. This has resulted in unprecedented success for companies like Reliance and Patanjali..

All economic activities including the most complex ones are finally aimed at consumption. However, to understand the kind of consumption that may be preferred by an individual, the concept of utility and indifference curve are extremely helpful.